Gridlocked: Planning Failure with the Southeastern Regional Transmission Planning Process12/20/2023 The Southeastern Regional Transmission Planning (SERTP) process is run by some of the largest utilities in the southeast, including Duke Energy, Southern Company, Tennessee Valley Authority and others. For the past decade, SERTP has failed to provide any real regional transmission planning solutions. SERTP was never intended to be a true planning process and is riddled with flaws. SERTP officially began in 2013 as an effort for the non-organized southeast to comply with the Federal Energy Regulatory Commission's newly minted Order 1000, which required improved regional transmission planning between utilities. The Department of Energy's latest National Transmission Needs Study found that the Southeast will need to expand its transmission capacity by 77% by 2035; however, even with the implementation of FERC Order 1000, this past decade has resulted in some of the lowest levels of investment in the Southeast compared to other regions around the country. An impediment described in the DOE report includes the lack of transparent locational energy pricing: "...information on the economic value of congestion outside RTOs/ISOs is minimal when compared with the market price differential data available from RTOs/ISOs..." As a result, "The Delta, Southeast, and Florida regions installed the fewest circuit-miles, relative to regional load, throughout the decade." Why does transparent locational energy pricing matter for transmission planning? In other regions, clear energy price differentials enable transmission planners to identify valuable transmission projects that would reduce overall system costs. Without energy pricing data, utilities in the south are effectively blindly managing generation dispatch to maintain system reliability, without consideration of ratepayer costs. There's always a cost, even if it's not accounted for.  This year, SREA worked with other stakeholders in the SERTP Regional Planning Stakeholders Group (RPSG) to develop four out of the five scopes of work for the "Economic Planning Study" process. SERTP is a transmission planning process entirely run by the utilities, and we were appreciative for the opportunity to develop several studies. The process works like this: identify a source (usually a full balancing authority area), an amount of megawatts to move (this is non-resource specific, so the models don't know if the new megawatts are solar or coal), and a sink where the power is moved to (again, another balancing area). Plug those data into the models, and the models help identify problems on the grid that need to be resolved. Based on some significant transmission constraints in Northern Georgia that were described by Georgia Power Company in their 2022 IRP, we evaluated moving 1.6 GW (in our view, solar projects) from Southern Georgia to Northern Georgia, and another scenario that looked for the same amount from TVA into North Georgia. The results were quite good. The SERTP utilities estimate $96 million in upgrades to move 1.6 GW of power from the South to the North of Georgia, and just $56.5 million to move that amount of power from TVA. Several of the transmission constraints (thermal loadings) are already exceeding 100% even without the requested new power flows (the Charleston-Hiwassee River 161 kV line is already at 108.7% thermal loading without any changes), indicating TVA's system is already stressed and the costs associated with the study results are not necessarily driven by the new power flows represented in the RPSG studies. When considering that transmission substations can easily cost tens of millions of dollars, these results are stunningly good. Speaking of TVA, we requested an evaluation of moving 2.9 GW of power from Arkansas (MISO South) into Memphis. A few years ago, Memphis Light Gas & Water evaluated leaving TVA and joining MISO. For MLGW, it would have necessitated building or contracting with about 2.9 GW of new generation resources in Arkansas. At the time, MLGW estimated the new transmission costs would have been close to $376 million. While MLGW paused its efforts to evaluate MISO membership, the SERTP results suggest TVA could easily bring in 2.9 GW of power for $21.5 million - about 94% less cost than MLGW calculated. Given TVA's recent blackouts during Winter Storm Elliott, the company ought to seriously consider these minor transmission upgrades. Finally, SERTP evaluated importing 1,242 MW of power from MISO North into Louisville Gas & Electric/Kentucky Utilities (LGEKU). That analysis was based on LGEKU's recent requests to the Kentucky Public Service Commission to replace some existing coal-fired power plants with new natural gas units. The company did not consider MISO imports as an alternative; however, in the SERTP process, we were able to evaluate potential transmission limitations. Again, the SERTP analysis found it would be relatively low cost to upgrade the transmission system and enable the power flows: just $83.5 million. Will any of these transmission projects get built? It all comes down to benefit metrics: how do transmission planners view the value of transmission compared to the costs? SERTP is Ineffective While the SERTP analysis results were quite positive, the extent of SERTP's usefulness ends with the study results. Stakeholders were shocked to learn that the SERTP utilities evaluate no benefit metrics for the potential projects identified. Thus, the "Economic Planning Studies" truly evaluate no economic component of transmission planning, nor do the studies incorporate even the most basic values of transmission. None of the transmission identified is guaranteed to be in the utilities' actual transmission plans. There is a process where SERTP utilities can evaluate a benefit of transmission. SERTP, by its tariff rules, is only allowed to evaluate a single benefit metric: avoided transmission. If the SERTP utilities find a transmission project that they like in the SERTP process, they would evaluate any savings associated with cancelling potentially smaller planned projects nearby. By replacing smaller transmission projects with a more robustly planned project, the utilities would theoretically reduce costs and build the new line. But there are a few problems with this theory. First, SERTP only evaluates 10 years’ worth of benefits from the time the study begins. Thus, if a study begins in 2024, the analysis will only stretch out to 2034/2035. SERTP utilities often insert the new transmission assumptions perhaps 5-9 years into the process, meaning that potentially only a few years of transmission benefits are calculated. Put another way, if a transmission project gets added in the 9th year of a 10-year model, only 1-year of benefits are measured, even though transmission projects can easily last 40-60 years and provide numerous benefits during that time. The time horizon is unreasonably short. Next, many utilities may have 10-year transmission plans; however, those same plans are typically most accurate for the first five years, with the later years not fully vetted. In this case, a transmission project is only evaluated after year 7 or 8 in the model, but the utilities' internal plans effectively only go to year 5. Therefore, no transmission would be avoided by the new proposed line. There are no benefits to measure. SERTP's shell-game has never led to new transmission being built. This year, the SERTP utilities opted to not even bother to perform this additional analysis. It's no wonder why the SERTP process has never led to any regional or interregional transmission development. The process was designed to fail from the beginning. SERTP Isn't Accurate Transmission planning incorporates two fundamental data sets: generation and load (power demand). By modeling where new generation will be installed, or older generation will be retired, in addition to any load growth or decline, transmission planners are meant to find any potential reliability problems caused by the ever-changing system. Once the problems are identified, solutions can be built. In SERTP, the participating utilities share data with neighboring utilities - a sort of data swap to ensure that one utility's plans aren't going to negatively affect someone else’s in the footprint. If utilities aren't sharing accurate data, transmission modeling will not be able to identify potential problems ahead of time. Recently, LGEKU received approvals from the Kentucky Public Service Commission to retire nearly 600 MW of coal, build a 640 MW of new natural gas capacity, as well as build nearly 800 MW of solar plus 125 MW/500 MWh of battery storage. In essence, LGEKU is undergoing some pretty dramatic changes over the next few years. However, LGEKU representatives told their SERTP neighbors that the utility expects no "change throughout the ten-year planning horizon for the 2024 SERTP Process." (slide 188). When asked about this discrepancy, LGEKU representatives stated that the solar facilities had not yet received their Generation Interconnection Agreements, despite being approved by the PSC, and so the company (using their own internal "best practices"), decided to not include those changes. By the way, LGEKU is in charge of its own generation interconnection process and approvals, so any delays are caused by the company itself. Duke Energy in the Carolinas performs a different type of analytical gymnastics. The company there knows it wants to retire some existing generation resources, like Cliffside 5, Marshall 1 & 2, Roxboro and Mayo. When transmission planners remove electric generation in the models, the entire system responds to those retirements by ramping up generation elsewhere. This change in the power flow can result in transmission constraints: problems that need to be solved. Instead of letting the models work, Duke inputs "proxy" generators into the model to make up for the retirements. Duke explains that through this process, "Generators [are] left in [the] model in expectation of replacement generation through the Generation Replacement Request process." In other words, the model is told there is no retirement and are unable to identify if any problems would arise from the retirements. This is a form of hardwiring power plants into the model. By hardwiring “no change” into the models, it biases transmission planning towards the status quo and increases the likelihood that a utility will install a natural gas unit. Observant readers would note here that Duke has not received state regulatory approvals to replace those specific units at those specific sites and includes the changes anyway, while LGEKU has received approvals but does not include the changes in their models. When asked about the discrepancy in which units to include versus exclude, the SERTP utilities explained that each utility comes up with their own methods of data reporting. The individual utility methodologies are not consistent. This "best practice" method evidently also extends to load growth projections as well, meaning state integrated resource plans (which include both generation and load assumptions) are not necessarily included in the SERTP process. Perhaps the most egregious lack of data transparency and transfer in SERTP is with the Tennessee Valley Authority. Like LGEKU, TVA reported to its SERTP neighbors that the company expects no changes over the next decade (slide 261). In May 2023, TVA CEO Jeff Lyash told his board of directors that after a successful competitive solicitation, the company plans to sign contracts for 6,000 megawatts of clean energy resources from 40 solar farms. Those contracts would go a long way to meeting TVA's own goal of adding 10,000 megawatts of solar by 2035. Meanwhile, TVA told the North American Electric Reliability Corporation (NERC) that the company will "add 7,251 MW of natural gas generation and retire 5,159 MW of coal generation over the period. A total of 3,937 MW of [Bulk Electric System]-connected Tier 1 solar PV projects are expected in the next 10 years." TVA is telling its Board of Directors (its regulators), NERC, and SERTP utilities three different stories over the next ten years. When asked about these discrepancies, SERTP utilities explained that each utility comes up with its own methodologies for sharing data, or not. There are no rules regarding what gets included, or not. SERTP Ignores Public Policy As part of the SERTP process, stakeholders are allowed to ask that the utilities include a public policy scenario. Stakeholders are required to file their scenario request 60 days after the Q4 meeting, usually about a month before the Q1 meeting the following year. In 2023, three public policy requests were filed by stakeholders regarding North Carolina's Carbon Plan, a legally binding state public policy. At the Q1 2023 meeting, stakeholders were told that the SERTP utilities were still "evaluating" these requests and would provide an update at the next meeting. At the Q2 2023 meeting, SERTP utilities explained that they would not be performing a public policy analysis because, "SERTP itself has no role in the North Carolina local transmission planning process." In effect, the SERTP utilities have eliminated any state public policy for future discussions. In its order adopting the Carbon Plan, the North Carolina Utilities Commission stated that, "Furthermore, based upon the potential magnitude of future transmission expenditures, the Commission urges Duke to explore all possible efficiencies and to be vigilant in its participation in SERTP and in its coordination with PJM to assure a least cost path to achieve the carbon dioxide emissions reduction requirements while maintaining and improving reliability." Evidently Duke can unilaterally ignore its regulators, and the SERTP public policy process, and stakeholders have no recourse. To date, roughly a decade after FERC Order 1000 outlined a role for including state public policy in transmission planning, SERTP has never modeled a public policy scenario. Fixing SERTP SERTP exists because of FERC Order 1000, requiring regional coordination in transmission planning. In recent years, FERC has again taken up the prospect of developing a more holistic regional planning effort. FERC's proposed regional transmission planning rule, if applied to non-RTO regions like the southeast, would greatly improve SERTP's planning process. The planning rule borrows some of the (true) best practices of other regions by requiring multi-scenario, multi-value (benefits) analysis. Unsurprisingly, utilities in the southeast opposed FERC's proposed transmission planning rules, arguing in part that because the states do IRPs and SERTP works fine, FERC should not impose the transmission rule on the southeast. SREA's comments to FERC call into question the validity of the IRPs and SERTP. Given that even IRPs are not directly included in SERTP (nor public policies, nor some state approved contracts), it appears that the SERTP utilities had not been entirely straightforward with FERC. The SERTP utilities also told the Department of Energy to ignore the region. The utilities told the DOE Transmission Needs Study team that, “SERTP Sponsors also disagree with the Study’s claims that the Southeast will need a lot more transmission capacity in the future, as it does not have enough evidence to support this assertion. SERTP Sponsors claim that the Southeast already has a strong transmission system and has been investing in it to meet the needs of customers and to accommodate state energy policies.” However, the DOE Needs Study found that the Southeast has been one of the lagging regions in transmission development in the country. While a new FERC transmission planning rule that applies to the southeast would be exceptionally helpful, the rule only applies to a few utilities in the southeast. Duke, LGEKU, OVEC, and Southern Companies are considered the "Jurisdictional SERTP Sponsors", while Associated Electric Cooperative Inc. (“AECI”), Dalton Utilities (“Dalton”), Georgia Transmission Corporation (“GTC”), the Municipal Electric Authority of Georgia (“MEAG”), PowerSouth Energy Cooperative (“PowerSouth”), and the Tennessee Valley Authority (“TVA”) are all non-jurisdictional utilities. Those utilities participate in SERTP voluntarily and are outside FERC’s jurisidiction. For utilities like TVA, their board of directors would need to get serious about their job as regulators and require TVA to engage in SERTP earnestly. Alternatively, the United States Congress could amend the TVA Act of 1935 and require that TVA become FERC-jurisdictional. Absent FERC or congressional action, state regulators have an important role to play. Based on SREA's experience with SERTP over the years, it was rare for any state regulatory agency to ever attend SERTP meetings. When we mentioned this lack of regulatory oversight at SERTP, regulators often lamented not having enough time, nor enough qualified staff to engage in the transmission planning forum. While both may be true, it only underscores the importance of having robust stakeholder engagement. Stakeholders can sometimes help fill in the information sharing gaps and alert regulators to contradictory behaviors. State regulators no longer have the luxury of ignoring SERTP or the transmission planning processes of their utilities. The North Carolina Utilities Commission recently pushed for a series of transmission planning reforms. The reformed the North Carolina Transmission Planning Collaborative will soon become the Carolinas Transmission Planning Collaborative. There, the CPTC includes "...the Multi-Value Strategic Transmission (MVST) planning process. The MVST process 1) adopts a forward-looking/ proactive approach, 2) uses a scenario based approach to account for different possible futures, 3) accounts for multiple benefits, 4) avoids line-specific assessments and piecemeal planning, and 5) allows for meaningful stakeholder input into the process." Many of these requirements are based off the FERC proposed transmission planning rule. The process includes a Transmission Advisory Group (TAG) for stakeholders to be engaged. However, if stakeholders propose a scenario that "is more Regional in nature", stakeholders are pointed back to filing a request in SERTP. Individual states can make great strides in improving their own backyard transmission planning rules, but the regional and interregional aspects of transmission planning in the southeast are still entirely dependent on broken SERTP process. To fully fix SERTP, a Multi-Regulatory Strategic Planning Process is needed that includes FERC, Congress, and the State PSC's towards a shared goal of a more robust grid. AuthorSimon Mahan is the Executive Director of the Southern Renewable Energy Association.

0 Comments

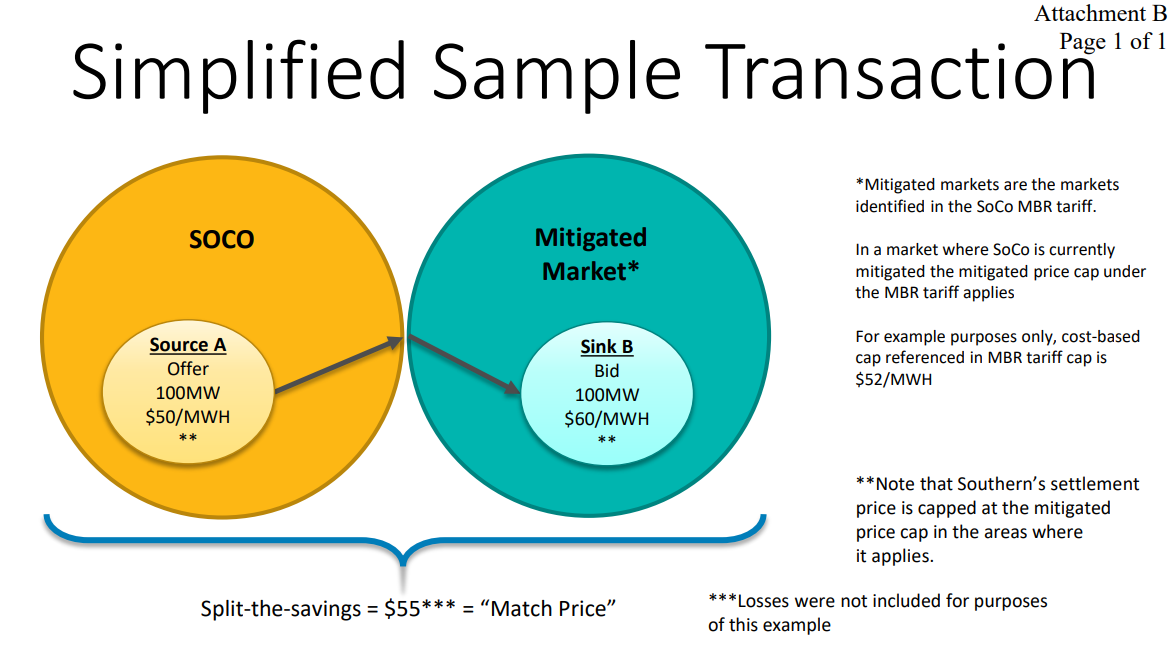

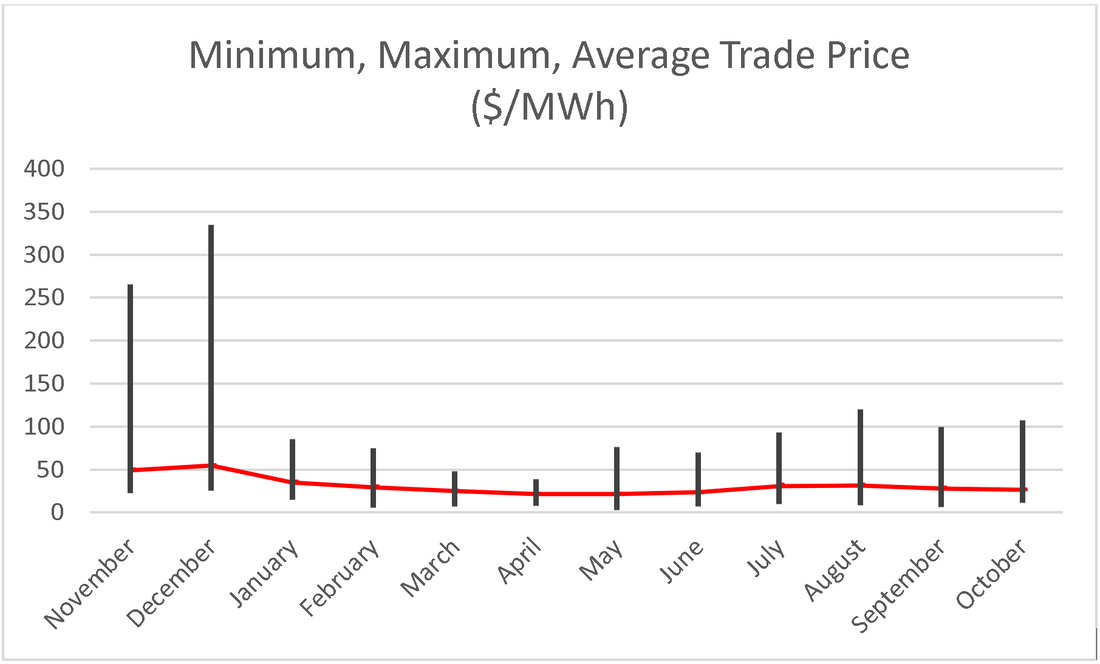

The Southeastern Energy Exchange Market (SEEM) began public operations on November 9, 2022. SEEM utilities touted it as an “Advanced Bilateral Market Platform” fit for the 21st Century. An early press release stated, “The result will be cost savings while improving the integration of all energy resources, including renewables, which are expanding rapidly in the Southeast, leading to a cleaner, greener, more robust electricity system.” Fans of broader regional market reforms, and opponents to SEEM, called the platform a “nothing burger” noting its paltry benefits. Over the past twelve months, SEEM utilities and opponents have been waiting to see if this experiment is a success or a failure. After a year’s worth of data and operations, it is fair to say that SEEM has not lived up to any of its promises.  A Small, Simple Market SEEM participants describe the platform as a simpler, easier, cheaper way to enable power flows across the southeast. Duke Energy and Southern Company have been two lead proponents of the market design. Testimony and analysis filed by the SEEM utilities at the Federal Energy Regulatory Commission (FERC) suggested utilities could save about $45 million annually with SEEM, or about $2/MWh of power traded. That is the same as just $0.002 per kilowatt hour (kWh) of electricity savings. For comparison, the Midcontinent Independent System Operator (a competing market structure) estimates it saved its members over $4 billion in 2022 alone, or nearly 100x more than SEEM was estimated to save. The premise is this: utilities would voluntarily offer extra energy on free transmission for a voluntary price, and if there is a voluntary buyer willing to pay a higher price, those two utilities would “match” and split the savings. SEEM participants provided this example: Southern Company wants to sell 100 megawatts (MW) of power for $50 per megawatt hour (MWh), and if a buyer is willing to purchase at $60/MWh, the two would split the price at $55/MWh and both end up better off than they would have been without the transaction. Below is an example of this sort of power trade.  This past year, very little power has been traded using SEEM. In total, 616,398 MWh of power were bought and sold over a twelve-month period. If an average home uses about 12,000 kilowatt hours (12 MWh) per year, the power traded on SEEM equates to about 51,000 homes. For comparison, a large-scale solar facility (300 megawatts) provides enough power for about 55,000 homes per year. Average power prices on SEEM were about $30/MWh, with minimum prices reaching $2.85/MWh in May 2023, and maximum power prices reaching $334.66/MWh in December 2022.  A Failed Market SEEM participants touted economic savings by engaging in this new platform. Testimony filed at the Federal Energy Regulatory Commission pegged gross benefits of $47 million annually, with an initial startup cost of $3.8 million, and annual operational costs of about $2.8 million. In a region with over 50 million people, SEEM was projected to save less than $1 per person per year. This past year’s operation has fallen well short of expectations and SEEM may not have saved any money this past year.  SEEM does provide some data publicly, but transparency is lacking. Buried deep in the SEEM public data is cell Z4 of the Public Monthly Informational Report spreadsheet, listing a “Total Benefit” value. There are no units, nor further description in any of the monthly Independent Market Auditor reports of what this value fully entails. However, this value likely represents the gross benefits created in the region for each month, given that gross benefits (as opposed to net benefits) are how SEEM’s value was described to FERC. The aggregated Total Benefits for the past year add up to $3.3 million—93% lower than the projected $47 million. If SEEM’s first year costs were $6.6 million ($3.8 million in startup costs, plus $2.8 million in operational costs, as estimated to FERC), and its gross savings were just $3.3 million, SEEM has cost southeastern ratepayers more than it has saved. Without full cost and benefit transparency from the SEEM utilities, these sorts of comparisons will remain difficult. In October 2023, the SEEM Board of Directors met and received an update from the Independent Market Auditor, Bob Sinclair of Potomac Economics. Three items of interest were included. First, “Large percentage of bids and offers are too far apart to clear.” Put another way: utilities are not submitting bids high enough, or offers low enough, for trades to occur. This is an unsurprising outcome, given that each bid and offer is entirely voluntary and not directly tied to specific generation. Next, “To match more efficiently bids need to come up and offers need to come down.” In other words: utilities are stingy when buying and tight-fisted when selling. Finally, “Clearing prices have strong correlation to gas market prices.” Solar is not a price driver. Gas is. The Auditor’s report notes that “The market is not highly liquid”. And “SEEM receives a substantial volume of uneconomic bids and offers that are unlikely to clear.” If the market is not functioning properly, the benefits that were described to FERC in SEEM’s original filings (and hoped for by participating utilities) as justification for the new market evaporate. SEEM is not operating as expected. A Dirty Market When SEEM participants filed their application at FERC, renewable energy was a top selling point. In the testimony provided, analysts stated, “It should be noted that the Southeast EEM can help participants manage periods of excess energy and high net demand ramping created by renewable integration.” SEEM utilities worked hard publicly to support SEEM as a valuable market for solar power generation, even stating, “The SEEM reduces carbon emissions and supports renewable energy integration…” In an alternative market structure like an RTO, power bought and sold is tied to specific generation resources, so buyers can determine exactly the type of resources being purchased. Not so in SEEM: power prices are totally separated from generation type, making it impossible to determine the exact resource mix being traded, or impact on emissions. It was important for SEEM’s branding, at least publicly, to appear to help solar power and reduce emissions. The reality is, of the few trades that have occurred on SEEM, SEEM has mostly been used at night, when solar power is unavailable. Data available on the SEEM website includes Public Hourly Available Transmission Capacity (ATC) Usage. Those data can be used to determine trade quantities and hours. It can also be used to determine which utilities are using the most ATC. Put another way, ATC is a way to measure which utilities are providing their transmission (for free) for electrons to zip across the region. ATC data cannot be used to determine buyers and sellers, nor can it determine generation type. During the night (7PM-7AM), the average Available Transmission Capacity used in each quarter hour was higher than the average used during daylight others (7AM-7PM). The top three hours of average transmission usage were 6AM, 1AM, and 11PM. The bottom three hours of average transmission usage includes 9AM and 8AM. SEEM’s generation mix at night is mostly coal, natural gas, and nuclear power—not solar power. There also appears to be no carbon emission accounting associated with SEEM, meaning the reduction in carbon emissions and support for renewable energy is without supporting data.  A Dysfunctional Market Based on the available data, some interesting market strategies appear. For instance, Participant O tends to keep its bids and offers around 10 MWh. Participant E prefers bigger slugs of power: 35 MWh for both bids and offers. Participant T keeps their bids and offers around the 1-2 MWh range. While the quantities are interesting, the pricing tactics are wild. Normal market operations suggest utilities would desire to buy low and sell high, or prices would be close to actual costs. That’s not always the case with SEEM. Participant O’s average bid purchase prices are often around $26/MWh and sale offer prices are around $31/MWh; a fairly tight window of low bids and high offers. Participants F, H, R, and T, on average, are bidding high and sell offers low. This may be an indicator those utilities are relying on SEEM as a market of last resort—as opposed to ramping down generation, sell low, and as opposed to buying longer term contracts, buy high. The stingiest utilities (the ones willing to pay the least for purchases) are Participant I (with an average bid of just $16.5/MWh), Participant B ($19.2/MWh), and Participant A ($22/MWh). If those participants are rational, those utilities must believe that their avoided costs are at least that low, and their generation units are more efficient than every other market participant. They are not seriously interested in buying power. One would expect these utilities to also set the lowest prices for offers, to out-compete their neighbors. But the opposite seems true: Participants I and B offer power for sale at a significant premium compared to their bid prices ($42/MWh and $35/MWh, respectively).  The high rollers are Participant R (with an average bid of $50.4/MWh), and Participants K and F (both around $34/MWh). A rational utility that bids high prices is likely very interested in purchasing power and will want to ensure the market makes a match. That may be because their existing generation fleet is relatively expensive, or scarce. One would expect a rational utility to create offers that are close in price to their existing generation (high bids, high offers). Strangely, Participants F and R have their average offers at a significantly lower level than their average bids—they plan to sell very low and buy very high. Participant R on average offers power to be sold at $19/MWh, but average bids for purchase are $50.4/MWh. Meanwhile, Participant M only wants to sell power at an average of $52/MWh, and never put in a bid to buy power. In the study submitted to FERC to support SEEM’s formation, one of the underlying assumptions is that “The study assumes that participants are submitting bids and offers at true costs. The impact of more complex bidding strategies was not accessed [sic].” The actual operational data suggests that utilities are not relying on their true costs to form bids and offers. A Desperate Market Perhaps there are temporal considerations at play—market participants could simply be withholding their bids and offers until a voluntary time that, based on some internal company belief or strategy, provides a value to their companies. During Winter Storm Elliott, when the only utilities in the nation to experience blackouts and rolling load shedding events were SEEM members, SEEM did not help. The Independent Market Auditor’s report from December 2022 showed that from December 24-26, no “matches” (trades) occurred. Offers (sales) almost entirely evaporated. That might not be terribly unusual: the region was struggling to provide power, so few utilities inside the SEEM footprint had “spare” energy to sell neighbors. Outside the SEEM market, MISO helped bail out the southeast by pumping gigawatts of power into the south. The truly bewildering outcome of Winter Storm Elliott was that the total SEEM bids (utilities with the desire to purchase power), plummeted. In a stressed power market, with presumably high-power prices, you would expect the market participants to increase their willingness to buy, and to increase both bid prices and bid quantities submitted. The opposite occurred. SEEM was not useful during Winter Storm Elliott, and the market participants appear to have abandoned it in the most extreme time. Participant O made 77% of the bids from December 24-25. The next most active participant during the storm was Participant G, with just 10% of bids submitted. Participants E, I, and L stopped participating entirely: no bids, no offers. Participant O also submitted the highest bid price of all time for SEEM during Winter Storm Elliott: $4,354.75/MWh. These prices were submitted as a bid at 11AM on December 24, 2022. The next highest bid prices were just $1,175/MWh by Participant K, around the same time. Clearly both of those utilities felt a strong need to boost their bid prices in the hopes of finding spare megawatts. In one aspect, the SEEM utilities determined it was cheaper for the lights to go off than bid higher prices and attract supplies (in the industry, this may be considered a soft version of a Value of Lost Load). No purchases nor sales were made on SEEM on December 24th, despite the high prices and the region’s rolling blackouts. Around that same lunchtime hour, solar power in the region was performing exceptionally well.  Bid prices are rarely high in the SEEM market, and similarly bids are rarely below zero. Only Participant A submitted a handful of negative bids this past year, and all in late April 2023. Given that no offers were ever made at a negative price, it is likely impossible these orders ever matched (bid prices must always be higher than offer prices). The lowest offer price was submitted by Participant H: $1/MWh for sale in both February and May 2023 for about 13 MWh to 25MWh at a time. When a utility offers power for nearly free prices in SEEM (or, even below operational costs), it is unclear how its ratepayers are impacted. These costs are obscured in utility rate cases with little to no transparency. A Discriminatory Market Some spectators have noted SEEM appears to be an elaborate public relations effort to discourage real market reform in the southeast, like developing an energy imbalance market (EIM) or a fully developed regional transmission organization (RTO). With minimal benefits, restricted governance, lackluster transparency, and no planning components, SEEM lacks many of the same attributes of a developed market. There is also no venue for state regulatory agencies (Public Service Commissions) to participate in SEEM, unlike RTOs where state regulatory involvement is guaranteed. On July 14, 2023, the DC Court of Appeal s released a decision regarding SEEM: the market is discriminatory. “The creation of a new service that—by its design—excludes existing market participants evokes the discriminatory practices against third party competitors by monopoly utilities that prompted the Commission’s adoption of Order No. 888,” the court said. The Federal Energy Regulatory Commission (FERC) is now required to reinvestigate the value of SEEM and determine if it is “…actually superior to the status quo in light of Order No. 888’s open access principles.” FERC has not acted on the remand order, yet. The future of SEEM is in limbo. The Path Forward Multiple studies have found that the southeast could benefit from broader market reform, like an energy imbalance market (EIM) or a regional transmission organization (RTO). These common-sense market reforms are operational throughout the United States. EIM’s and RTO’s are tried and tested market structures that rely less on highly speculative model results to create benefits. Alternatively, SEEM’s entire foundation was built on an assumption that participants would be active and rational; neither has proven to be true. During Winter Storm Elliott, the southeast relied heavily on neighboring RTOs to help keep our systems afloat. Each year that the southeast waits to determine whether SEEM might live up to its promises is another year of millions of dollars in lost benefits. It is time our state regulators take the reins on SEEM, investigate its operations, and plan for a better system. AuthorSimon Mahan is the Executive Director of the Southern Renewable Energy Association. |

ArchivesCategories |

RSS Feed

RSS Feed